August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Review of Pacific Basin Financial Markets and Policies, Vol. 4, No. 2 (2001) 235–264 c World Scientific Publishing Company

Dynamic Modeling of Stock Market Interdependencies: An Empirical Investigation of Australia and the Asian NICs Abul M. M. Masih School of Finance and Business Economics, Edith Cowan University, Perth WA 6027, Australia E-mail:

[email protected] Rumi Masih Emerging Markets Economic Research, Goldman, Sachs and Co., New York, NY 10004, USA and Faculty of Economics and Politics, University of Cambridge, Cambridge CB3 9DD, England This article examines the patterns of dynamic linkages among national stock prices of Australia and four Asian NIC stock markets namely, Taiwan, South Korea, Singapore and Hong Kong. By employing recently developed time-series techniques results seem to consistently suggest the relatively leading role of the Hong Kong market in driving fluctuations in the Australian and other NIC stock markets. In other words, given the generality of the techniques employed, Hong Kong showed up consistently as the initial receptor of exogenous shocks to the (long-term) equilibrium relationship whereas the Australian and the other NIC markets, particularly the Singaporean and Taiwanese markets had to bear most of the brunt of the burden of short-run adjustment to re-establish the long term equilibrium. Furthermore, given the dominance of the Hong Kong market in the region, the study also brings to light the substantial contribution of the Australian market in explaining the fluctuations to the other three markets, particularly Singapore and Taiwan. Finally, in comparison to all other NIC markets, Taiwan and Singapore appear as the most endogenous, with the former providing significant evidence of its short-term vulnerability to shocks from the more established market such as Australia. Keywords: Australia, emerging/established stock market, linkages, cointegration.

1. Introduction Recently, much effort has been devoted to understanding the patterns of dynamic linkages and interdependencies across national stock market 235

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

236 • A. M. M. Masih & R. Masih

[Schollhammer and Sand (1985), Eun and Shim (1989), Smith et al. (1993), Brocato (1994), Chowdhury (1994), Kwan et al. (1995)]. Moreover, closely related to this issue have been works attempting to shed light on the nature of the propagation mechanism driving stock market fluctuations, particularly in light of the latest stock market crash of October 1987 [King and Wadhwani (1990), Malliaris and Urrutia (1992), Arshanapalli and Doukas (1993), Masih and Masih (1997)]. While a number of these studies have focused on national equity markets of industrial countries which have by now fundamentally established markets, it would be of some interest to analyse the dynamic fluctuations (in terms of lead-lag relationships) of the emerging stock markets, located primarily in the NICs of East Asia. It is the purpose of this paper to study the dynamic inter-linkages of national equity markets of four such markets, namely Taiwan, South Korea, Singapore, Hong Kong and Australia.1 These markets are not only important to Australia in terms of growing economic interdependence but also of regional interest (i.e. Asia-Pacific Rim versus northern hemisphere OECD). In this regard, we do not intentionally consider Japan but aim to present a regional exposition of how the dynamics of these Asian emerging markets (EM) is propagated and whether these linkage patterns change in response to the movements of a more established market such as Australia. During the last decade, the phenomenal growth of the Asian NICs, their gradual lifting of barriers to foreign capital, the privatisation of some of their public utilities, and their potential to influence the transmission mechanism underlying global stock market fluctuations warrant such a study at the regional level which has not been explored yet with the application of recent appropriate techniques. Most studies that have attempted to investigate lead-lag relationships [Cheung and Mak (1992), Malliaris and Urrutia (1992), Arshanapalli and Doukas (1993), Smith et al. (1993), Chowdhury (1994), Brocato (1994), Kwan et al. (1995)] have, due to data limitations or methodological drawbacks, used simple bivariate lead-lag relationships among two markets, or standard Granger F -tests in a VAR framework which are only useful in 1

Note that International Finance Corporation (IFC) classifies only Korea and Taiwan as “emerging markets”. Therefore in this analysis, if taken literally in the context of the IFC definition, Hong Kong and Singapore do not constitute “emerging markets”. Digressing from a definitional debate regarding “emerging” and “non-emerging market” and for the sake of convenience in this study, when referring to the emerging Asian NIC markets, we include Hong Kong and Singapore in the same breath.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 237

capturing short-run temporal causality [Granger 1986]. While examinations of bivariate relationships may provide additional insight, they are not entirely useful for purposes of policy and serve at best as a pre-requisite for a more thorough analysis of relationships among stock markets in a multivariate setting. While much of the previous research stress the need to test for the number of common stochastic trends [Kasa (1992), Blackman et al. (1994)], we extend the analysis by using Vector Error-Correction Models and Generalised Impulse Response/Variance Decompositions [see Masih and Masih (2001,1999] in order to gain insight into the short- and long-run leadlag or causal relationships among the international stock markets.2 The dynamic VECM representation provides us with a framework to test for the temporal causal dynamics (in the Granger sense) among the stock price markets through both short-run and error-correction channels of causation [see Granger (1986), (1988)]. Prior to this, we test for unit roots using a comprehensive pre-testing. In order to quantify the VECM results of leadlag relationships and gain further insight into the strength of such causal directions, forecast error variance decomposition analysis is undertaken. Furthermore, the dynamic response path of an unanticipated shock from an established stock market to the NIC markets is traced out over time to provide a visual illustration of the influence of market vulnerability. Finally, implications for the propagation or transmission mechanism of the causal responses are addressed in addition to discussing in what way this formulation may be used in understanding the interdependent and dynamic linkages underlying international share markets. This particular study has a regional focus covering Australia and the NICs prompted by their heavy interdependencies through trade and investment and cross-listing of stocks and also the more common monetary policy followed by them due to their linkages with the USA as one of the major trading partners and their currencies being tied to the US dollar. The analytical framework it has to offer, however, may be particularly relevant to a broader examination of international globalisation of stock markets. 2

While the VECM is an extension, in that it accounts for any underlying cointegrating restrictions through the imposition of error-correction terms, it is a facet of VAR modelling. Modelling techniques in the VAR vain have already been applauded as an effective means of characterising the dynamic interactions among economic variables by reducing dependence on the potentially inappropriate theoretical restrictions of structural models [see Lastrapes and Korhay (1990) and McMillin (1991)].

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

238 • A. M. M. Masih & R. Masih

This paper is organised in the following manner: a background to the wide-ranging literature surrounding this issue, the theoretical arguments underlying investigations of stock market interdependencies, and a brief summary of the recent growth and characteristics of emerging markets (EMs) are provided in Sec. 2; an introduction to the stock price data, the econometric techniques, methodology and approach to modelling are presented in Sec. 3; Sec. 4 provides a very brief description of the data prior to presenting and discussing estimation results in further detail; a summary, broad but major implications for policy and conclusions of the study are made in Sec. 5. 2. Background Literature, Theoretical Underpinnings and Emerging Stock Market: Recent Trends and Characteristics 2.1. Literature review From the vanguard of gauging the propagation mechanism of stock markets in general, work has mainly centred around testing for the number of common stochastic trends underlying a system of stock prices. This approach was popularised by Kasa (1992) who used an error-correction model to compute common stochastic trends for equity markets of five countries (US, Japan, England, Germany, Canada). Presenting evidence of a single stochastic trend underlying the equity markets of these countries, point estimates of factor loadings suggested that this trend is most important in the Japanese market and the least important in the Canadian market. Complementing this approach, Chung and Liu (1994) examined common stochastic trends among national stock prices of the US and five East-Asian economies and Corhay et al. (1993) tested for the number of common stochastic trends in European stock markets. Others have used alternative methods in order to search for co-movements in international equity markets [see Hilliard (1979) in an application of spectral analysis; Eun and Shim (1989) who found evidence of several interdependent linkages amongst national stock prices; Chowdhury (1994) for an investigation of stock market interdependencies in four Asian newly industrialised economies who use ordinary VARs and daily data but over only five years; and the latest of which is a study by Kwan et al. (1995) whose analysis covers a wide array of international stock markets but is restricted to testing weak form of speculative market efficiency and employ Granger bivariate causality tests]. More recently, Blackman et al. (1994) examined whether there existed any long-term statistical relationships between monthly prices of shares

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 239

on different national industrialised share markets. Using a split-sample approach before and after the development of global markets, their evidence supported the case of long-term relationships during the post-globalisation period (January 1984 to February 1989). This led them to suggest that any profit from diversification of shares across national borders were not as high in the post-globalisation period as they were in the pre-globalisation period. Similar to this study Corhay et al. (1995), examined the long-run relationship among five major Pacific-basin stock markets, and found that within this integrated area, regional aspects such as Asian versus the Pacific play significant roles. Using an alternative ARCH approach, Hamao et al. (1990) found significant support for growing integration among three major international stock markets of the US, Japan and UK. While these are important findings, what may be of even more importance and interest, particularly to analysts in Australia, is the behaviour of stock market fluctuations of the Asian NICs, particularly since the early 1980s and how the advent of their growth influenced, if at all, the propagation mechanism generating index movements of the Australian stock market. 2.2. Theoretical underpinnings In the context of market integration and interdependencies, there have been numerous studies that have focused on this issue though, more often than not in the context of developed stock markets. One important implication of integrated markets is that assets associated with a similar level of risk and/or liquidity will lead to a similar level of return regardless of the location or country of investment. This issue has been empirically addressed in several studies [see Errunza and Losq (1985), Jorian and Schwartz (1986) and Hietala (1989)], as well as placed under critical scrutiny due to inconsistent results [see, inter alia, Wheatly (1988) who argues that even without market integration, assets that are diversified internationally could be “mean-variance efficient”]. The integration and interdependence of stock markets underlies a major cornerstone of modern portfolio theory which addresses the issue of diversifying assets. In essence, this theme advocates investors to diversify their assets across national borders, as long as returns to stock in these other markets are less than perfectly correlated with the domestic market. The advantages of asset diversification have already been widely discussed in the literature in which much effort was devoted to attempts that quantify risk-reduction and its associated benefits available to the internationally

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

240 • A. M. M. Masih & R. Masih

diversified portfolio [see Grubel (1968), Lessard (1973), Agmon and Lessard (1977), Solnik (1991) and references therein]. Closely tied with this issue is that stock prices tend to move closely together and upward trend over time. Kasa’s (1992) finding of a unique common stochastic trend in a system of five stock markets held implications that these markets were perfectly correlated over the long-run (although there could be significant deviations over the short-term). In this respect, the analytical tool of cointegration lends itself quite conveniently to investigating the long-run relationships of stock market movements. 2.3. Asian emerging stock markets: Recent trends and characteristics In the global financial context, one of the most dramatic events which have unfolded over the previous decade has been the massive growth of emerging stock markets, in particular those of the NIEs under consideration in this analysis. At the end of 1992, these four markets, as a group, had a significant stake in the near 11 times growth of total capitilization of EMs as a whole (alternatively a tripling of EM share of global equity market capitilization, from 2.5 percent to 7 percent). The growth experience of EMs could also be shown by the almost 25 times increase of trading volume from 1982 to 1992, escalating the listed trading companies in these markets to approximately 40% of worldwide companies. These dramatic movements in trends of EMs meant that during the latter half of the 1980s, EMs as a group were outperforming the markets of the OECD. There have been numerous reasons postulated for this rapid growth in these markets. Firstly, Governments in less developed countries and in NICs in particular, have become more liberal in adopting market-oriented policies geared to privatise previously public enterprises such as transport and communications and public utilities; secondly, financial sectors in these countries have been opened to foreign private sector investment; thirdly, the corporate sectors are now becoming increasingly competitive in these countries, even on an international level; NIC state-owned enterprises continue to become more privatised, paving the way for shares being distributed among a wider span of the population; finally, these markets are increasingly becoming more attractive to international investors and financiers due to their escalating future growth potential — this especially has resulted in a greater number of companies trading and added further fuel to participatory attraction and

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 241

incentive for foreign investors due to the EMs’ ongoing liberalization and relaxing of previously closed-door regulations, particularly in such markets as Korea.3 The future potential of corporate earnings in these markets is also looking very healthy. Underlying the growth in the financial sector is of course the higher rate of economic growth these countries are experiencing. This in itself is likely to translate into more solid corporate growth and higher returns. EMs are also likely to offer a far greater diversification potential for attracting global portfolios. The International Financial Corporation reports that while individual emerging markets have been quite volatile, as a group their risk-adjusted return has superseded that of the developed markets.4 Given the potential of these markets, it would be useful to address the characteristics of each of these NIC markets. Chowdhury (1994) provides a good appraisal of these markets treating Hong Kong and Singapore as a subgroup, since in comparison to the others they are the most open markets, which is not surprising given their free-trade principles governing economic policies. In comparison to Singapore, the Hong Kong stock market enjoys a relatively unrestricted, almost a totally free-access operating environment and has hence attracted a large participatory regional and international financial audience. In terms of the extent of non-barrier access, the Singapore market is the next best in which institutional arrangements partially limit opportunities. The Korean and Taiwanese markets are the focus of worldwide attention since they are opening up to foreign participation. Although the Korean market is still affected by regulatory operating policies and the Taiwanese market is prone to domestic financial inefficiencies and volatility, once some of the reforms discussed above are firmly in place, the fruits of multi-tiered liberalization should result in these markets dominating regional influences. In terms of market capitalization, the Korean and Taiwanese 3

Reforms have been targeted on three separate levels: firstly there have been wider-ranging institutional reforms appealing to the domestic community and international investors, such as stock exchange modernization, the establishment of central clearing and settlement corporations and depositories, a reduction in commission rates and transaction fees, more insider trading rules and financial auditing practices; secondly financial system reforms that are encouraging the introduction of new institutional investors such as private insurance and pension funds; thirdly reforms to adopt wider financial instruments in providing potential investors with broader choice of markets, by example in the NICs with futures and options markets. 4 Given these developments, international portfolio investment in the EMs has grown to an astronomical figure of $50 billion at the end of 1992.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

242 • A. M. M. Masih & R. Masih

markets alone now constitute $208.5 billion of total global capitalization and are among the 15 largest in the world superseding several markets of the developed world. 3. Econometric Methodology 3.1. Cointegration and Granger (temporal) causality The cointegration technique pioneered by Engle and Granger (1987), Hendry (1986) and Granger (1986), made a significant contribution towards testing Granger-causality.5 According to this technique, if two variables are cointegrated, the finding of no-causality in either direction — one of the possibilities with the standard Granger (1969) and Sims (1972) tests — is ruled out. However, although cointegration indicates the presence or absence of Granger-causality, it does not indicate the direction of causality between variables. This direction of the Granger (or temporal) causality can be detected through the vector error correction model derived from the long run cointegrating vectors. 3.2. Vector Error-Correction Modelling (VECM) and multiple causal channels Engle and Granger (1987) demonstrated that once a number of variables (say, xt and yt ) are found to be cointegrated, there always exists a corresponding error-correction representation which implies that changes in the dependent variable are a function of the level of disequilibrium in the cointegrating relationship (captured by the error-correction term) as well as changes in other explanatory variable(s).6 5

Causality is a subject of great controversy among economists. See, for example, Zellner (1988). Interested readers could refer to a supplementary issue of the Journal of Econometrics, September-October, 1988, that includes studies discussing this issue. Without going into a debate, we would like to state that the concept used here is in the stochastic or “probabilistic” sense, rather than in the philosophical or “deterministic” sense. Also the concept used here is in the Granger “temporal” sense, rather than in the “structural” sense. 6 The VAR being a system of unrestricted reduced form equations, have been criticised by Cooley and Le Roy (1985). Runkle (1987) is a good example of the controversy surrounding this methodology. Backus (1986) and Ambler (1987) are examples defending the use of VAR. It is debatable whether the method of identification employed by the simultaneous equation structural model which often relies on many simplifying assumptions and arbitrary exclusion restrictions together with the related exogenous-endogenous variables classification (which are often untested) is superior to the identification procedure used in

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 243

In addition to indicating the direction of causality amongst variables, the VECM approach allows us to distinguish between “short-run” and “longrun” forms of Granger-causality. When the variables are cointegrated, in the short-term, deviations from this long-run equilibrium will feed back on the changes in the dependent variable in order to force the movement towards the long-run equilibrium. If the dependent variable (say, the change in the Korean stock price index) is driven directly by this long-run equilibrium error, then it is responding to this feedback. If not, it is responding only to short-term shocks to the stochastic environment. The F -tests of the “differenced” explanatory variables give us an indication of the “shortterm” causal effects, whereas the “long run” causal relationship is implied through the significance or otherwise of the “t” test(s) of the lagged errorcorrection term(s) which contains the long term information since it is derived from the long run cointegrating relationship(s). The coefficient of the lagged error-correction term, however, is a short-term adjustment coefficient and represents the proportion by which the long-run disequilibrium (or imbalance) in the dependent variable is being corrected in each short period. Non-significance or elimination of any of the “lagged error-correction terms” affects the implied long-run relationship and may be a violation of theory. The non-significance of any of the “differenced” variables which reflect only short-run relationship, however, does not involve such violations because typically theory has little to say about short-term relationships [Thomas (1993)]. The novelty of this technique can be illustrated in testing various economic issues which are elusive with respect to the causal direction. By example, this technique or formulation has also been used in mainstream macroeconomic analysis in order to test for the causal chains implied by the major paradigms in macroeconomic theory [see Masih and Masih (1995) and Masih, R. and A. Masih (1996)]. 3.3. Variance Decompositions (VDCs) and Impulse Response Functions (IRFs) The VECM, F - and t-tests may be interpreted as within-sample causality tests. They can indicate only the Granger-exogeneity or endogeneity of the the VAR model. The critics of VAR, however, all agree that there are important uses of the VAR models. For example, McMillin (1988) points out that VAR models are particularly useful in the case of “forecasting, analyzing the cyclical behaviour of the economy, the generation of stylized facts about the behaviour of the elements of the system which can be compared with existing theories or can be used in formulating new theories, and testing of theories that generate Granger-causality implications.”

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

244 • A. M. M. Masih & R. Masih

dependent variable within the sample period. They do not provide an indication of the dynamic properties of the system, nor do they allow us to gauge the relative strength of the Granger-causal chain or degree of exogeneity amongst the variables beyond the sample period. VDCs, which may be termed as out-of-sample causality tests, by partitioning the variance of the forecast error of a certain variable (say, the Korean market) into proportions attributable to innovations (or shocks) in each variable in the system including its own, can provide an indication of these relativities. A variable that is optimally forecast from its own lagged values will have all its forecast error variance accounted for by its own disturbances [Sims (1982)].7 The information contained in the VDCs can be represented equivalently by IRFs. Both are obtained from the moving average (MA) representation of the original VAR model.8 IRFs essentially map out the dynamic response path of a variable (say, the Taiwanese market) due to a one-period standard deviation shock to another variable (say, the Australian market). 4. Data and Estimation Results 4.1. Data The data is comprised of end-of-month closing share price indexes of the four NIC stock markets: Taiwan (T N ), South Korea (SK), Singapore (SG), Hong Kong (HK) and Australia (AU S) over the period January 1982 to 7

The results based on VARs and VDCs are generally found to be sensitive to the lag length used and the ordering of the variables. A considerable time has been spent in selecting the lag structure through FPE criterion. FPE method is based on an explicit optimality criterion of minimizing the mean squared prediction error. The criterion tries to balance the risk due to bias when a low order is selected, and the risk due to increase in the variance when a higher order is selected. By construction, the errors in any equation in a VAR are usually serially uncorrelated. However, there could be contemporaneous correlations across errors of different equations. These errors were orthogonalised through Choleski decomposition. 8 The impulse response functions like the variance decompositions were also obtained from the unrestricted VAR form of the model, although they could be computed via a dynamic multiplier analysis of VAR systems with cointegration constraints [see Lutkepohl (1993) and Lutkepohl and Reimers (1992)]. To trace the dynamic effects of various shocks, the estimated VECM is reparameterized to its equivalent formulation in levels. With this reparameterization, the error-correction terms are incorporated into the first-period lagged terms of the autoregression. The model is then inverted to obtain the impulse response functions that capture the effects of deviations from long-run equilibrium on the dynamic paths followed by a variable in response to initial shocks. Intuitively, IRFs trace the response over time of a variable, say x, due to a unit shock given to another variable, say y. A similar procedure is adopted, among others, by Robertson and Orden (1990).

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

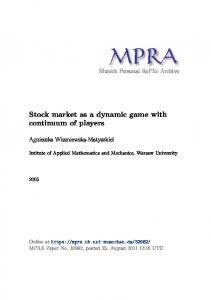

Dynamic Modeling of Stock Market Interdependencies • 245 7.5 S.Korea

7

Taiwan

6.5

Log of SPI

6 Australia 5.5 5 Hong Kong

4.5 4 3.5

Singapore

Fig. 1. 1994)

Jul-93

Jan-94

Jul-92

Jan-93

Jan-92

Jul-91

Jul-90

Jan-91

Jul-89

Jan-90

Jul-88

Jan-89

Jul-87

Jan-88

Jul-86

Jan-87

Jul-85

Jan-86

Jul-84

Jan-85

Jul-83

Jan-84

Jul-82

Jan-83

Jan-82

3

Aggregate Stock Markets of Australia and Asian NICs (January 1982 to June

June 1994. All data have been sourced from various issues of International Financial Statistics published by the International Monetary Fund.9 The aggregate stock price indexes representing the four NIC markets and Australia are depicted graphically over the period of this analysis in Figure 1. Incidentally, these NIC markets were also those examined in an analysis by Chowdhury (1994) adopting a much shorter but higher frequency sample data-set. 4.2. Unit root tests with a changing mean over full sample In the following we conduct several tests to determine the univariate integrational properties of the stock prices and perform a series of unit root tests prior to testing for multivariate cointegration. The five stock price indexes are graphically depicted in Figure 1. The impact of the October 1987 crash is clearly apparent with stock indexes declining by an average of 7.42 per cent in just between one month’s trading (September to October 1987). Given the visual significance displayed in Figure 1 and the possibility that the crash altered the structure of stock prices in general, we employ a test suggested by Perron (1990) to test for a series with a changing mean. This test allows a single-time shift in the structure of the time series at time TB with (1 < TB < T ) where T is the 9

Consistent with others in the literature [Kasa (1992), King, et al. (1994)] the raw indexes have been transformed to reflect real US dollars in order to adopt the prerspective of the US investor.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

246 • A. M. M. Masih & R. Masih Table 1. Market HK TN SK SG AUS

Perron’s Full Sample Unit Root Tests with Changing Mean

µ

t(µ)

γ

t(γ)

δ

t(δ)

α

t(α)

−0.149 −0.351 −0.036 −0.199 −0.616

−1.617 −2.331 −0.317 −1.467 −0.801

−0.034 −0.120 −0.029 −0.021 −0.031

−1.367 −1.851 −0.763 −1.213 −2.185

−0.568 −0.625 −0.052 −0.538 −0.568

−7.021 −4.438 −0.706 −9.171 −11.769

1.031 0.929 1.017 0.959 1.019

−1.845 −2.178 −0.484 −1.413 −1.151

Notes: Variables represent the aggregate national stock market price index for Hong Kong (HK), Taiwan (TN), South Korea (SK), Singapore (SG) and Australia (AUS). All t-stats test the null that the parameter is equivalent to zero except t(α) which is a t-test with H0 : α = 1. The critical value for the distribution of t(α) for λ = 0.5, T = 150 at the 5% level is −3.39 [Perron (1990)]. Sample: 1982:01 to 1994:06.

sample size. In the context of our analysis, TB is chosen to be the month of the crash. The test is based on the regression: yt = µ + γDt + δD(T B)t + αyt−1 +

k X

cj ∆yt−j + εt

(1)

j=1

where Dt = 0 if t < TB and 1 otherwise; TB equals the period 1987:10 (the 70th observation for the full sample of 150 total observations) in which the crash took place; T = 150; D(T B)t = 1 if t = (TB + 1) and 0 otherwise; and ∆ is a difference operator. The ratio between TB and T , λ, is equivalent to 0.467. According to Perron (1990, Table 4, p. 158), the critical value for T = 150 and λ = 0.5 at the 5 percent level of significance is −3.36 for the distribution of t(α) . Estimation results of this regression for each stock price index are presented in Table 1. Observing the values for t(α) , it is clear that we cannot reject the null hypothesis that there exists a unit root in any of the SPIs under consideration at the 5 per cent level of significance.10 4.3. Other tests for univariate integration: Tests of the unit root hypothesis Various other unit root testing procedures, ranging from the classical DickeyFuller (DF) test [see Dickey and Fuller (1979, 1981)] to Sims’ Bayesian test 10

We also conducted tests provded by Banerjee-Lumsdaine-Stock and variants of other similar sequential testing procedures discussed in the July 1992 special issue of Journal of Business and Economic Statistics, which are immune to the criticism that the Perron tests require prior knowledge of a break point. None of these tests, which are not reported due to further space coverage, showed significant evidence to contest these findings.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 247

[Sims (1988)], were also applied to test for the order of integration for each of the SPIs over the full sample.11 First, these tests were applied with the SPIs in levels, followed by the same tests in their first difference form [see Appendix Table A1]. Our results that each of these SPIs are non-stationary processes in level form, but stationary in their first-differences, are supportive of similar findings in the literature [Kasa (1992), Blackman et al. (1994)]. In order to confirm that the variables are not integrated of higher orders, Dickey and Pantula (1987) tests which are used for testing the presence of one or more unitary roots at the zero frequency, were also conducted in addition to various other tests. These tests could not significantly reject the null hypothesis that all SPIs were I(1).12

4.4. Multivariate cointegration tests Given the common integrational properties of the SPIs, the next stage in the analysis is to test for the presence of cointegration in the fivedimensional vector of stock prices: [AUS, HK, TN, SK, SG]. In this analysis, we employ the Johansen and Juselius (JJ) procedure of testing for multiple cointegrating vectors. Unlike its predecessor, the JJ procedure poses several advantages over the popular residual-based Engle-Granger two-step approach in testing for cointegration. Specifically, they may be summarised as follows: (i) the JJ procedure does not, a priori, assume the existence of at most a single cointegrating vector, rather it explicitly tests for the number of cointegrating relationships; (ii) unlike the Engle-Granger procedure which is sensitive to the choice of the dependent variable in the cointegrating regression, the JJ procedure assumes all variables to be endogenous; (iii) related to (ii), when it comes to extracting the residual from the cointegrating vector, the JJ procedure avoids the arbitrary choice of the dependent variable as in the EngleGranger approach, and is insensitive to the variable being normalised; (iv) the JJ procedure is established on a unified framework for estimating and testing cointegrating relations within the VECM formulation; (v) JJ provide the appropriate statistics and the point distributions to test hypothesis

11

A summary of these test statistics and their corresponding equations are available upon request. 12 Since none of the additional testing procedures conducted provided results to contest our earlier finding to any significant extent, due to space, we do not report these results as part of this article, though they are certainly available upon request from authors.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

248 • A. M. M. Masih & R. Masih Table 2.

Johansen and Juselius’s Tests for Multiple Cointegrating Vectors

Long-Run Cointegrating Vector

Hypotheses

[AUS, HK, TN, SK, SG]

H0 : r r r r r

=0 ≤1 ≤2 ≤3 ≤4

H1 : r r r r r

>0 >1 >2 >3 =5

Test Statistics Max Eigenvalue 35.63∗∗ 22.11 14.38 9.38 0.12

Trace 81.62∗∗ 45.99 23.88 9.50 0.12

Tests of Zero Restrictions on Coefficients of JJ Long-Run Cointegrating Vectors Hong Kong 5.21∗∗

Taiwan 3.00∗

S. Korea 7.48∗∗∗

Singapore 3.29∗

Australia 9.61∗∗∗

Notes: The optimal lag structure for each of the VAR models was selected by minimising the Akaike’s FPE criteria. Critical values are sourced from Johansen and Juselius (1990). ∗∗ indicates rejection at the 95% critical values. The test statistic under the null hypothesis is distributed as chi-square with 1 degree of freedom. ∗∗∗ , ∗∗ and ∗ denote significance at the 1%, 5% and 10% levels, respectively.

for the number of cointegrating vectors and tests of restrictions upon the coefficients of the vectors.13 The JJ procedure involves the identification of rank of the 5 by 5 matrix Π in the specification given by: ∆Xt = δ +

k−1 X

Γi ∆Xt−i + ΠXt−k + εt

(2)

i=1

where, Xt is a column vector of the five SPIs. If Π has zero rank, no stationary linear combination can be identified. In other words, the variables in Xt are non-cointegrated. If the rank is r, however, there will now exist r possible stationary linear combinations. Results of applying the Johansen-Juselius procedure, using an optimal lag structure for the VAR, are presented in Table 2. Both the maximum eigenvalue and trace statistics indicate that there exists at most a single 13

With respect to both the Engle-Granger and JJ approach, it is important to acknowledge that should non-cointegration not be rejected at conventional significance levels,it is possible that the residual term may display fractional behaviour and still be meanreverting implying fractional cointegration. For such an approach see Masih and Masih (1998) and R. Masih and A. Masih (1995).

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 249

cointegrating vector, i.e. r = 0 is rejected by the 95 per cent critical values, but this is not true for the null of r ≤ 1. While an optimal lag selection criteria was employed in choosing the lag length of the VAR, both the maximum eigenvalue and the trace statistic appeared to be robust to at most r = 1 across alternative lag lengths. Given the presence of one cointegrating vector, we may conclude that there exists (n − r) = 4 common stochastic trends among this system of national stock market prices. The finding of cointegration among these five markets has several implications. Firstly, it rules out “spurious” correlations and also the possibility of Granger non-causality which in turn implies at least a unique channel for Granger causality to emerge (either uni-directional or bi-directional). Secondly, the actual number of cointegrating (or equilibrium) relationship(s) found in Table 2 will result in a corresponding number of residual series and hence error-correction terms (ECTs) which we may embed as exogenous variables appearing in their lagged-levels as part of the vector error-correction model (VECM) in Table 3. Thirdly, cointegration also rules out the use of modelling any dynamic relationships through ordinary first-differenced VARs as these will be misspecified, and also ordinary structural VARs [see Rogers and Wang (1993) for applications], as these models do not impose Table 3.

Summary of Tests of Temporal Causality Based on VECM

∆AUS

∆HK

Dep Variable ∆AUS ∆HK ∆TN ∆SK ∆SG

– 0.99 1.72 0.48 1.14

∆TN

∆SK

∆SG

F -statistics 0.22 – 0.05 0.65 1.88∗

1.62 1.44 – 0.54 1.91∗

ECT[εi,t−1 ] t-statistic

0.87 0.86 3.85∗∗∗ – 0.90

1.13 1.58 1.16 2.37∗∗ –

−2.19∗∗ −0.21 −2.72∗∗∗ −1.73∗ −3.58∗∗∗

Notes: The ECTs (εit−1 for i = 1) for each model were derived by normalising the cointegrating vectors on AUS, resulting in r number of residuals. Figures that appear in the final column are estimated t-statistics testing the null that each lagged-ECT is statistically insignificant. All other estimates are asymptotic Granger F -statistics. The residuals used in constructing the ECTs (from the JJ-VAR) were also checked for stationarity by way of unitroot testing procedures applied earlier and inspection of their autocorrelation functions respectively. The VECM was estimated using an optimally determined criteria (Akaike’s FPE) lag structure for all lagged-difference terms and a constant. ∗∗∗ ∗∗ , , and ∗ indicates significance at the 1%, 5% and 10% levels.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

250 • A. M. M. Masih & R. Masih

cointegration constraints.14 These and many other related issues are discussed by King et al. (1991) and Toda and Phillips (1993) who support the use of VECMs in empirical tests of Granger causality. 4.5. Long-run cointegrating vectors and tests of zero loading restrictions Having established the presence of a single cointegrating vector, the Johansen and Juselius procedure allows us to test several hypotheses on the coefficients by way of imposing restrictions and likelihood ratio tests which are, asymptotically, chi-square distributed with one degree of freedom. Scrutinising the cointegration vector in each model, presents us with a measure of the most important component, in terms of its relative weight, in comparison to the remaining components. Coefficient estimates and significance levels associated with the tests of zero-loading restrictions appear below tests for multivariate cointegration appearing in Table 2. An interesting observation is that each of these markets enters their respective cointegrating vectors in a statistically significant fashion (note that SPI=0 is rejected at least at the 10 percent level). In general, these results suggest that almost all markets adjust in a significant fashion to clear any short-run disequilibrium. 4.6. Temporal causality and vector error-correction modelling Given the presence of a unique cointegrating vector in the five-dimensional VAR used in the JJ cointegration tests, this then provides us with one errorcorrection term for constructing models. Analogously, we may also extract (n − r) or 4 common trends, [for such an approach see Kasa (1992), Chung and Lui (1994)]. The VECM provides us with some interesting results. Results are presented in Table 3 which indicates that, the Australian market, along with Taiwan, Korea and Singapore, are all endogenous with respect to the 14

Wang et al. (1994) is another example of an application of a structural VAR model with imposed long-run restrictions based on theoretical predictions of endogenous consumption, labour-leisure and fertility. However, in order to arrive at the structural VAR, various univariate and multivariate stationarity tests were performed on the data. However, as noted by Karras (1994, p. 1768), “If cointegration relationships are found to exist, the model must be estimated by the Vector Error Corrections Model (VECM) examined by Engle and Granger (1987) and more recently used by King et al. (1991).”

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 251 Table 4. Summary of Short-Run Lead-Lag Linkages among Australian and Asian NIC Stock Markets

AUS

TN

SG

SK

HK

Notes: X → Y indicates that changes in X contains leading information for changes in Y (i.e. changes in X Granger causes changes in Y, or changes in Y lags or is influenced by changes in X). X ← Y implies the reverse. A dashed (—) line indicates absence of a causal linkage. Symbols in bold-italics (X) indicate that the(se) market(s) bears the burden of shortrun adjustment to the long-run equilibrium relationship, implied by the VECM.

statistical significance of the error correction term. In fact, the only market which remains statistically exogenous, is the NIC market of Hong Kong. This model also suggests that, with the exception of Hong Kong, all other markets are to some degree endogenous. Short-term linkages, as indicated in Table 4, run from Korea to Taiwan, Singapore to Korea, Taiwan and Hong Kong to Singapore. Note that although Australia does not exert any significant influence on the NIC markets in the short-term, the novelty of the VECM shows that it does share linkages with most of these Asian markets through the error-correction channel of causality. In summary, the VECMs revealed that the NIC market of Hong Kong seems to be unambiguously econometrically exogenous, while the Singapore stock market seems the most prone to short and long-term channels of linkages from other markets in the area. The emerging markets of Taiwan and Korea, which are also by comparison the most restricted, appear to be the most prone to short-term fluctuations from other markets. Cointegration among these five markets need some explanations. One might also wonder whether the presence of cointegration among these markets is related to any systematic risk factors driving these markets. It seems to us that first of all, there were the effects of globalisation factors common to all these countries in different degrees, such as, increase in financial deregulations, technological innovations, financial product innovations, cross-listing of stocks of multinationals, and macro-economic policy coordinations among

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

252 • A. M. M. Masih & R. Masih

G-7. In addition, there were a couple of factors binding Australia and the four Asian NICs in particular. These NICs were increasingly dependent on the regular supply of Australia’s agricultural and mineral resources in particular, to feed their growing industrialisation process. Australia in return had to accommodate their growing exports of manufactures. For example, during the mid-1980s to mid-1990s, the share of Asian NICs in goods exports from Australia went up from around 10 percent to 22 percent and the share in goods trade during the same period jumped from 22 percent to almost 33 percent.15 This significant interdependency in trade got reflected in their stock market linkages as well. Moreover, greater linkages among these countries are also due to the more common monetary policy followed by them, particularly since the October crash. All these countries have the USA as one of the major trading partners and most of their currencies are tied to the U.S. dollar. In fact, the exchange rate pegging became much stronger after the crash. The standard deviation of the exchange rate between the US dollar and each of these countries’ currency fell (after the crash) by a substantial amount [see Rogers (1994)]. Given the growing stock market linkages among these five markets, it is no wonder that the regional leader was Hong Kong followed by Australia as evidenced in our statistical results. This is quite intuitive and can be explained in terms of the extent of the equity market capitalisation (which is indicative of the liquidity of the market), and the extent of deregulations and openness of the economy (which affects the transaction costs involved). 4.7. Diagnostic tests on VECM Since the VECM was estimated by OLS and our test statistics may be prone to inconsistencies due to non-spherical disturbances, a battery of diagnostic tests were applied for each equation covering departures from serially uncorrelated errors, homoskedastic error variances, non-autoregressive conditional and heteroskedastic errors, normally distributed errors, well-specified functional form. In general, with the exception of normality at the 10 percent level of significance for the Australian ECM, all these tests, given the power for which they are designed over the sample, could not find any significant evidence of departures from standard assumptions.16 15

Australian Bureau of Statistics, International Merchandise Trade, Australia, December Quarter, 1996, Catalogue 5422.0, 58-59 16 A full set of results of diagnostic tests for each equation of the VECM is available upon request from authors.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 253

4.8. Variance Decompositions (VDCs) and causal relativities Although the VECM (as noted in Sec. 3), provides us with a rich, dynamic framework for which temporal causality may be tested, they are strictly within-sample test. In order to gauge the relative strength of the variables or to “quantify our temporal causality results”, we now shock the system of stock markets and partition the forecast error variance of each of the markets. The decomposition results are presented in Table 5, for 5 alternative accumulative months, although only those results pertaining to 24 months after the shock are discussed. Looking through the main diagonal, we may ascertain the extent to which a variable is exogenous since this represents how much of a market’s variance is being explained by movements in its own shock over the forecast horizon. In a statistical sense, if a variable explains most of its own shock, then it does not allow variances of other variables to contribute to it being explained and is therefore said to be relatively exogenous. The important issue here is that the decomposition analysis is a relative exercise and results from it should be interpreted with this in mind. The decomposition analysis presented in Table 5 indicates a substantial degree of cross contributions. Clearly, however, in terms of the own shock being explained, the Hong Kong market illustrates its relative exogeneity with over 82 per cent of own variances being explained by its own innovations. Consistent with our results from the VECM, the Hong Kong market stands out as the most exogenous, followed by the Australian and other NIC markets. The contribution of the Australian market though is pre-eminent across fluctuations in most markets with over a third of the relative variance in the Singapore market, and almost a fifth of the relative variance in the Taiwan market being explained by shocks to the Australian market. In terms of the most endogenous market and once again consistent with results from the VECM, Singapore appears to be the most dependent upon other markets with approximately 57 percent of its relative variance being explained by shocks to other markets. 4.9. Unanticipated shocks and impulse response analysis An equivalent representation of VDCs are through impulse responses, which in the context of our analysis, provide the dynamic response of each variable to innovations of this variable as well as of other variables included in the system. In other words, impulse response functions portray to what extent the shock of one market is transitory (or persistent) in terms of its effect on the other markets in the system. In order to illustrate the usefulness of this

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

254 • A. M. M. Masih & R. Masih Table 5.

Decomposition of Variance

Percentage of Forecast Variance Explained by Innovations in: ∆AUS Mths 1 3 6 12 24

∆HK

∆TN

∆SK

∆SG

00.00 10.17 10.71 16.11 16.19

0.00 3.76 5.26 5.39 5.38

0.00 0.01 2.04 4.37 4.40

0.00 1.26 3.14 3.83 3.94

91.02 86.05 81.58 82.35 82.02

0.00 3.92 6.62 7.37 7.33

0.00 0.97 3.38 5.02 5.16

0.00 2.20 3.67 5.28 5.60

1.38 1.60 1.82 2.22 2.57

92.46 76.59 70.54 61.89 61.17

0.00 5.01 6.55 12.46 12.51

0.00 0.38 1.69 5.39 5.52

1.58 12.59 13.77 15.00 15.00

0.87 0.82 1.90 2.15 2.18

96.09 74.16 63.10 60.76 60.42

0.00 0.71 8.79 8.59 8.74

8.44 9.54 11.60 12.39 12.67

1.08 2.79 4.66 5.15 5.16

1.70 1.69 2.85 4.45 4.52

51.77 49.89 45.03 43.30 43.03

Relative Variance in: ∆AUS

100.00 84.79 78.85 70.29 70.09

Relative Variance in: 1 3 6 12 24 Yrs 1 3 6 12 24

∆HK

8.98 6.85 4.74 9.98 9.89

Relative Variance in: ∆TN

6.17 16.42 19.40 18.05 18.21

Relative Variance in: 1 3 6 12 24

∆SK

1.47 11.71 12.45 13.50 13.65

Relative Variance in: 1 3 6 12 24

∆SG

37.01 36.10 35.85 34.71 34.63

Notes: Figures in the first column refer to horizons (i.e. number of months). All other figures are estimates rounded to two decimal places — rounding errors may prevent a perfect percentage decomposition in some cases. Several alternative orderings of these variables were also tried — such alterations, however, did not alter the results to any substantial degree. This is possibly due to the variance-covariance matrix of residuals being near diagonal, arrived at through Choleski decomposition in order to orthogonalise the innovations across equations.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 255 4.50E-02 4.00E-02 3.50E-02 Taiwan Standard Deviations

3.00E-02 2.50E-02 2.00E-02

Singapore Hong Kong

1.50E-02 S. Korea

1.00E-02 5.00E-03 0.00E+00 -5.00E-03 1

2

3

4

5

6

7

8

9

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

-1.00E-02 Months After Shock

Fig. 2. Impulse Responses of Hong Kong, Singapore, South Korea and Taiwan Markets from a One-Standard Deviation Shock to the Australian Market

tool in providing further insights into the dynamic linkages of this system of stock markets, impulse responses of each NIC market are traced over time from a unitary standard deviation shock to the Australian market. The impulse responses are graphically portrayed in Figure 2 and illustrate that, apart from Korea, all markets respond with a fair degree of volatility, the most prominent are the fluctuations of the Taiwan stock market. Moreover, it takes the Taiwanese market almost eight months to settle after the initial impact of the shock. Our analysis indicates that, unlike the finding of Chowdhury (1994) who examined the linkages of the US and Japanese markets on these NIC markets, the Taiwan market does respond in a turbulent fashion to shocks from the Australian market. Korea on the other hand, similar to a finding by Rogers (1994) who notes the absence of any response of this market from the Japanese and US markets in particular, does not show any strong response in terms of volatility or persistence. This, to a certain extent, indicates that the Korean market is still ’closed’ in comparison to the other NIC emerging markets. 5. Summary, Policy Implications and Concluding Remarks There can be several motivations behind this analysis, ranging from a need to improve our understanding of the degree of integration shared by regional markets to further insights into knowledge of the propagation mechanism or dynamics driving these relationships. The necessity to undertake such an analysis to shed light on these issues becomes all the more relevant in light of

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

256 • A. M. M. Masih & R. Masih

the phenomenal growth and potential expansion of the Asian NIC markets. The substantial potential of trading power these markets are predicted to encapsulate over the present decade is in itself worthy of claim in significantly influencing, if not altering the transmission mechanism underlying global stock market fluctuations. In this paper, we have suggested and applied methods that allow for such analysis employing a multivariate, dynamic framework allowing for both short- and long-run relationships to manifest over time. In this respect some of the methodological deficiencies existing in previous studies in the literature, have to some extent been addressed. The concept of cointegration among a set of emerging stock markets in the Asian region was used to test whether they shared any degree of long-run integration with more established stock markets. The analysis was then extended to an investigation of the temporal causal dynamics of each of the stock market models through a dynamic vector error-correction modelling formulation. Since VECMs mechanically specify a formulation of dynamic linkages from a broad set of possibilities [see Tegene and Kuchler (1994)], they permit the data to express its driving forces without imposing any constraint by way of a specific structure. In this regard, VECMs provide a rich variety of procedures to be applied in testing temporal causal hypotheses [see King et al. (1991), Toda and Phillips (1993)]. Extensions to this model were also made in reference to assessing our within-sample tests by decomposing the forecast error variance from a once off shock to the system, into contributions of a market’s own and other markets’ variance, in explaining the shock over a time path. In summary, having established that all stock indexes are I(1) variables, our analysis from a multivariate VAR formulation significantly rejected noncointegration among all alternative sets of five stock price indexes. In the system of five stock markets we found evidence of one cointegrating vector, or equivalently four common stochastic trends. The residuals from these vectors were then embedded in a five-dimensional VECM that suggested that the Hong Kong market was clearly econometrically exogenous. The Hong Kong market firmly stood out as the initial receptor of any exogenous shock for the group of NIC markets and Australia. These results from the VECM were also broadly consistent with the variance decompositions (VDCs) which reconfirmed the relatively clear exogeneity of the Hong Kong market followed by the Australian market and the clear endogeneity of the Singaporean and Taiwanese markets throughout all cases. The policy implications of our dynamic analysis are quite clear. This study is an attempt at placing the analysis of stock markets in a temporal

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 257

Granger causal framework, by examining the relationship among four NIC markets and an important regional market of Australia. Put briefly, our results hold import for policy/investment considerations in the following ways: (i) The evidence of cointegration rules out the possibility of the estimated relationship being “spurious” and implies that Granger causality must exist in at least one direction. This finding is consistent with an intuitive notion of integration amongst these markets. In this regard, this study adds to the growing evidence of integration or comovements amongst international stock market prices. This, in itself, is a very important and valuable finding for assisting financial analysts who may use information optimally in acknowledging that these markets do not operate mutually exclusive to each other, nor in the presence of established markets. (ii) One of the implications from this analysis is that tests of the MEH and temporal causality, and studies of the propagation mechanism, whether be it in a stock market or any asset market, should be addressed in a multivariate and, if possible, cointegrated framework, particularly since the fluctuations in the financial markets are so interactive and interdependent. In addition, the existence of cointegration and Granger causality in at least one direction implies that one stock index will help in predicting the other. This can be interpreted by some as a violation of the market efficiency hypothesis. However, although from the presence of cointegration among these five stock markets our results are consistent with a violation of the market efficiency hypothesis, this should be evaluated with due caution, even if in a speculative sense. The evidence of cointegration implies that since each national stock price series contains information on the common stochastic trends (which bind all the stock market prices together), the predictability of one country’s stock prices can be enhanced significantly by utilizing information on the other countries’ stock prices. But does this predictability necessarily imply market inefficiency? Some years ago Granger (1986) argued that cointegration between (say) two prices implied an inefficient market because the error-correction model indicates that one or both prices are predictable. But we believe predictability implies nothing necessarily about inefficiency. A market is inefficient only if by using the predictability one could earn risk-adjusted excess returns. If returns could be generated, are they just compensation for risks or are truly excess and risk-adjusted? So one must be very careful in concluding that cointegration or a lack thereof necessarily implies anything about market inefficiency or efficiency. For more on this, one could see Dwyer & Wallace (1992) and Richards (1995).

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

258 • A. M. M. Masih & R. Masih

(iii) The evidence of cointegration has implications for portfolio diversification by international investors. Its presence implies that there is a common force (such as arbitrage activity) which brings these stock markets together in the long term. A test of cointegration, therefore, can also be said to be a test of the extent of the level of arbitrage activity in the long term. Since these markets are interdependent and highly integrated, they will act as if they are constituents of one integrated market. Hence the possibility of gaining abnormal profits in these markets through diversifying investment portfolios, is very limited indeed because in theory it is likely to be arbitraged away in the long term. In the absence of barriers, or potential barriers, of the kind that would justify country risk and exchange rate premiums, a highly integrated financial market would imply similar interest rates or expected yields for financial claims of similar risk and liquidity without any other regard to nationality or location (see von Furstenberg and Jeon, 1989). However, two qualifications should be added here. First, cointegration does not rule out the possibility of arbitrage profits through diversifying portfolios across these countries in the short term which may last for quite a while. Secondly, because of varying degrees of business and financial risks of different securities and also because of various security cash flows co-varying less than perfectly across different countries (and even within the same country), the diversification benefits in cointegrated markets in the long term may be reduced but are not likely to be fully eliminated in practice. (iv) The Granger-causal chain implied by our dynamic analysis (based on VECM and VDCs) tends to suggest that it was the Hong Kong market which more often predominantly led other markets, including Australia. In other words, the Hong Kong market was the initial receptor of exogenous shocks to its equilibrium relationship, and the other stock markets had to bear the burden of short-run adjustment (to the long-run trends) endogenously in different proportions in order to re-establish equilibrium. This finding could be attributable to two factors: (i) although the US market dominates global markets, the Hong Kong market is a dominant regional market and generator of influential information and therefore conducive to the public reaction hypothesis [see Becker et al. (1995)]; and (ii) international investors often overreact to news from dominant markets and place less weight on information from other markets. Assuming these overreactions on the part of traders are systematic, market linkages themselves may become further intensified by an accumulation of misspricing behavior being propagated amongst equity markets [see King and Wadhwani (1994) and follow up discussion by Poterba (1990)] within this region. Significant short-run linkages also appear

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 259

to run between the NICs, such as Korea to Taiwan, Singapore to Korea, Taiwan and Hong Kong to Singapore, though Singapore and Taiwan seem to be the most prone to other markets in establishing a relationship over the long-run. This is a major empirical finding, which contains both intuitive appeal and strong policy implications. (v) Finally, this analysis has brought to light the substantive crosscontributions of the Australian market in explaining the shocks to at least three of the four NIC markets. In particular, the impulse response analysis showed immediate and volatile response from the Taiwanese and the Singaporean markets in response to a shock to the Australian market. The greatest percentage of own variance being explained by own shocks, without itself being explained by any other market to any significant degree, was in the case of the Hong Kong market. The dominance of Hong Kong is plausible in view of its relative higher liquidity (given higher capitalisation and trading volumes) and lower transaction costs (given greater openness and deregulations of the economy). In this respect, although the story may be different when we account for more internationally active markets, this study provides fresh evidence of the dominance of the Hong Kong market in this region, as well as acknowledging that the Australian market does seem to have a substantial impact on other NIC markets in the region. Acknowledgments The authors would like to thank especially, without implication, Soren Johansen, Jesus Gonzalo, and the participants at the recent Annual Conference of Economists of the Economic Society of Australia and also at the Eighth Pacific Basin Finance, Economics and Accounting and the Second ADSGM International Conference, Bangkok, 2000, for their very helpful comments and discussions. Any errors, omissions or misinterpretations are accepted equally by the authors. The views expressed in this paper are not necessarily shared by Goldman, Sachs and Co., Goldman Sachs International, or any of its related offices. References Agmon, T. and D. Lessard (1977), “Investor Recognition of Corporate International Diversification”, Journal of Finance 32, 1049–1055. Ambler, S. (1989), “Does Money Matter in Canada? Evidence from a Vector Error Correction Model”, Review of Economics and Statistics 69, 651–658.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

260 • A. M. M. Masih & R. Masih

Arshanapalli, B. and J. Doukas (1993), “International Stock Market Linkages: Evidence from the Pre- and Post-October 1987 Period”, Journal of Banking and Finance 17, 193–208. Backus, D. (1986), “The Canadian-U.S. Exchange Rate: Evidence from a Vector Autoregression”, Review of Economics and Statistics 68, 628–37. Becker, K. G., J. E. Finnerty and J. Friedman (1995), “Economic News and Equity Market Linkages between the U.S. and U.K.”, Journal of Banking and Finance 19, 1191–1210. Blackman, S. C., K. Holden and W. A. Thomas (1994), “Long-Term Relationships between International Share Prices”, Applied Financial Economics 4, 297–304. Brocato, J. (1994), “Evidence on Adjustments in Major National Stock Market Linkages Over the 1980s”, Journal of Business Finance and Accounting, 643–667. Cheung, Y-L. and S. Mak (1992), “The International Transmission of Stock Market Fluctuations between the Developed Markets and the Asian-Pacific Markets”, Applied Financial Economics 2, 43–47. Chowdhury, A. R. (1994), “Stock Market Interdependencies: Evidence from the Asian NIEs”, Journal of Macroeconomics 16, 629–651. Chung, P. J. and D. J. Liu (1994), “Common Stochastic Trends in Pacific Rim Stock Markets”, Quarterly Review of Economics and Finance 34(3), 241–259. Cooley, T. F. and S. F. Leroy (1985), “Atheoretical Macroeconometrics: A Critique”, Journal of Monetary Economics 16, 283–308. Corhay, A., A. Tourani Rad and J.-P. Urbain (1993), “Common Stochastic Trends in European Stock Markets”, Economic Letters 42, 385–390. , (1995), “Long Run Behaviour of Pacific-Basin Stock Prices”, Applied Financial Economics 5, 11–18. Dickey, D. A. and W. A. Fuller (1979), “Distribution of the Estimators for Autoregressive Time-Series with a Unit Root”, Journal of the American Statistical Association 74, 427–431. , (1981), “Likelihood Ratio Statistics for Autoregressive Time Series with a Unit Root”, Econometrica 49, 1057–1072. Dickey, D. A. and S. G. Pantula (1987), “Determining the Order of Differencing in Autoregressive Processes”, Journal of Business and Economics Statistics 5, 455–461. Dwyer, G. J. Jr. and M. S. Wallace (1992), “Cointegration and Market Efficiency”, Journal of International Money and Finance 11, 318–327. Engle, R. F. and C. W. J. Granger (1987), “Cointegration and Error Correction: Representation, Estimation, and Testing”, Econometrica 55, 251–276. Errunza, V. and E. Losq (1985), “International Asset Pricing Under Mild Segmentation: Theory and Tests”, Journal of Finance 40, 105–124. Eun, C. and S. Shim (1989), “International Transmission of Stock Market Movements”, Journal of Financial and Quantitative Analysis 24, 241–256. Granger, C. W. J. (1969), “Investigating Causal Relations by Econometric Models and Cross Spectral Methods”, Econometrica 37, 424–438.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 261

, (1986), “Developments in the Study of Cointegrated Economic Variables”, Oxford Bulletin of Economics and Statistics 48, 213–228. , (1988), “Some Recent Developments in a Concept of Causality”, Journal of Econometrics 39, 199–211. Grubel, H. (1968), “Internationally Diversified Portfolio: Welfare Gains and Capital Flows”, American Economic Review 58, 89–94. Hamao, Y., R. Masulis and V. Ng (1990), “Correlation in Price Changes and Volatility Across International Stock Markets”, Review of Financial Studies 3, 281–307. Hendry, D., (1986), “Econometric Modelling with Cointegrated Variables: An Overview”, Oxford Bulletin of Economics and Statistics 48, 201–212. Hietala, P. T. (1989), “Asset Pricing in Partially Segmented Markets: Evidence from the Finnish Markets”, Journal of Finance 44, 697–718. Hilliard, J. (1979), “The Relationship between Equity Indices on World Exchanges”, Journal of Finance 34, 103–114. Johansen, S. (1988), “Statistical Analysis of Cointegration Vectors”, Journal of Economic Dynamics and Control 12, 231–254. Johansen, S. and K. Juselius (1990), “Maximum Likelihood Estimation and Inference on Cointegration with Applications to Money Demand”, Oxford Bulletin of Economics and Statistics 52, 169–210. Jorion, P. and E. Schwartz (1986), “Integration versus Segmentation in the Canadian Stock Market”, Journal of Finance 41, 603–616. Karras, G. (1994), “Sources of Business Cycles in Europe: 1960-1988. Evidence from France, Germany and the United Kingdom”, European Economic Review 38, 1763–1778. Kasa, K. (1992), “Common Stochastic Trends in International Stock Markets”, Journal of Monetary Economics 29, 95–124. King, M. A. and S. Wadwhani (1990), “Transmission of Volatility between Stock Markets”, Review of Financial Studies 3, 5–33. , E. Sentana and S. Wadhwani (1994), “Volatility and Links between National Stock Markets”, Econometrica 62, 901–933. King, R. G., C. I. Plosser, J. H. Stock and M. W. Watson (1991), “Stochastic Trends and Economic Fluctuations”, American Economic Review 81, 819–840. Kwan, A. C. C., A-B Sim and J. A. Cotsomitis (1995), “The Causal Relationships between Equity Indices on World Exchanges”, Applied Economics 27, 33–37. Lastrapes, W. D. and F. Korhay (1990), “International Transmission of Aggregate Shocks Under Fixed and Flexible Exchange Rate Regimes: United Kingdom, France and Germany, 1959 to 1985”, Journal of International Money and Finance 9, 402–423. Lessard, D. (1973), “International Portfolio Diversification: A Multivariate Analysis for a Group of Latin American Countries”, Journal of Finance 28, 619–633. Lutkepohl, H. (1993), Introduction to Multiple Time Series Analysis, (2nd ed.), Berlin: Springer-Verlag. Lutkepohl, H. and H-E. Reimers (1992), “Impulse Response Analysis of Cointegrated Systems”, Journal of Economic Dynamics and Control 16, 53–78.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

262 • A. M. M. Masih & R. Masih

Malliaris, A. G. and J. L. Urrutia (1992), “The International Crash of October 1987: Causality Tests”, Journal of Financial and Quantitative Analysis 27(3), 353–364. Masih A. M. M. and R. Masih (1995), “Temporal Causality and the Dynamic Interactions among Macroeconomic Activity within a Multivariate Cointegrated System: Evidence from Singapore and Korea”, Weltwirtschaftliches Archiv 131(2), Jun, 265–285. , (1997), “Dynamic Linkages and the Propagation Mechanism Driving Major Stock Markets: An Analysis of the Pre- and Post-Crash Eras”, Quarterly Review of Economics and Finance 37(4), Fall, 859–885. , (1998), “A Fractional Cointegration Approach to Testing Mean Reversion between Spot and Forward Exchange Rates: A Case of High Frequency Data with Low Frequency Dynamics”, Journal of Business Finance and Accounting (JBFA) 25(7) & (8), Sept/Oct, 987–1003. , (1999), “Are Asian Stock Market Fluctuations Due Mainly to Intra-Regional Contagion Effects? Evidence Based on Asian Emerging Stock Markets”, PacificBasin Finance Journal 7(3–4), September, 251–282. , (2001), “Long and Short Term Dynamic Causal Transmission amongst International Stock Markets”, Journal of International Money and Finance 20(4), August (forthcoming). Masih, R. and A. M. M. Masih (2001), “A Fractional Cointegration Approach to Empirical Tests of PPP: New Evidence and Methodological Implications from an Application to the Taiwan/US Dollar Relationship”, Weltwirtschaftliches Archiv. 131(4) (Dec), 673–694. , (1996), “Macroeconomic Activity Dynamics and Granger Causality: New Evidence from a Small Developing Economy Based on a Vector Error-Correction Modelling Analysis”, Economic Modelling 13(1), 407–426. McMillin, W. (1988), “Money Growth Volatility and the Macroeconomy”, Journal of Money, Credit and Banking 20, 319–335. , (1991), “The Velocity of M1 in the 1980s: Evidence from a Multivariate Time Series Model”, Southern Economic Journal 57, 634–648. Perron, P. (1988), “Trends and Random Walks in Macroeconomic Time Series”, Journal of Economic Dynamics and Control 12, 297–332. , (1990), “Testing for a Unit Root in a Time Series with a Changing Mean”, Journal of Business and Economic Statistics 8(2), 153–162. Phillips, P. C. B. and P. Perron (1988), “Testing for a Unit Root in Time Series Regression”, Biometrika 75, 335–346. Poterba, J. M. (1990), “Discussion (of King and Wadhwani paper)”, Review of Financial Studies 3, 34–35. Richards, A. J.(1995), “Comovements in National Stock Market Returns: Evidence of Predictability but not Cointegration”, Journal of Monetary Economics 36, 631–654. Robertson, J. and D. Orden (1990), “Monetary Impacts on Prices in the Short and Long Run: Some Evidence from New Zealand”, American Journal of Agricultural Economics 72, 160–171.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

Dynamic Modeling of Stock Market Interdependencies • 263

Rogers, J. H. (1994), “Entry Barriers and Price Movements between Major and Emerging Stock Markets”, Journal of Macroeconomics 16, 221–241. Rogers, J. H. and P. Wang (1993), “Sources of Fluctuations in Relative Prices: Evidence from High Inflation Countries”, Review of Economics and Statistics 75(4), 589–605. Runkle, D. E. (1987), “Vector Autoregression and Reality”, Journal of Business and Economic Statistics 5, 437–54. Schollhammer, H. and O. Sand (1985), “The Interdependence Among the Stock Markets of Major European Countries and the United States: An Empirical Investigation of Interrelationships Among National Stock Price Movements”, Management International Review 25, 17–26. Sims, C. (1972), “Money, Income, and Causality”, American Economic Review 62, 540–552. , (1982), “Policy Analysis with Econometric Models”, Brookings Papers on Economic Activity 1, 107–152. , (1988), “Bayesian Scepticism on Unit Root Econometrics”, Journal of Economics Dynamics and Control 12, 463–474. Smith, K. L., J. Brocato and J. E. Rogers (1993), “Regularities in the Data between Major Equity Markets: Evidence from Granger Causality Tests”, Applied Financial Economics 3, 55–60. Solnik, B. (1991), International Investments, New York: Addison-Wesley. Tegene, A. and F. Kuchler (1994), “Evaluating Forecasting Models of Farmland Prices”, International Journal of Forecasting 10, 65–80. Thomas, R. L. (1993), Introductory Econometrics: Theory and Applications, London: Longman. Toda, H. Y. and P. C. B. Phillips (1993), “Vector Autoregressions and Causality”, Econometrica 61(6), 1367–93. von Furstenberg, G. M. and B. N. Jeon (1989), “International Stock Price Movements: Links and Messages”, Brookings Papers on Economic Activity 1, 125–177. Wang, P., C. K. Yip and C. A. Scotese (1994), “Fertility Choice and Economic Growth: Theory and Evidence”, Review of Economics and Statistics 76(2), 255–266. Wheatley, S. (1988), “Some tests of International Equity Integration”, Journal of Financial Economics 21, 177–212. Zellner, A. (1988), “Causality and Causal Laws in Economics”, Journal of Econometrics 39, 7–21.

August 30, 2001

10:12

WSPC/155-RPBFMP

00040

264 • A. M. M. Masih & R. Masih

Appendix Table A6.

Tests of the Unit Root Hypothesis of Individual Stock Price Indexes

Aug Dickey-Fuller τµ

ττ

Phillips-Perron Z(α)

Z(tα )

Z(Φ1 )

Z(α∗ )

Z(tα∗ ) Z(Φ2 )

Z(Φ3 )

Sample: 1982:01 to 1994:06 Levels HK TN SK SG AUS

−0.03 −1.13 −0.72 −0.71 −1.42

−2.18 −1.37 −1.04 −1.65 −1.95

−0.11 −1.93 −0.71 −2.34 −2.66

0.06 −1.15 −0.70 −0.83 −1.42

1.20 1.66 3.40 0.92 2.24

−19.43∗∗ −4.55 −2.18 −15.73∗∗ −7.76

−2.55 −1.44 −0.99 −2.04 −1.96

3.41 1.42 2.44 3.22 2.20

−11.87 −11.11 −13.28 −10.62 −12.33

46.69 41.07 58.99 37.43 50.71

5.87∗ 1.14 0.53 4.25 2.08

First Differences (∆) HK TN SK SG AUS

−4.87 −3.69 −3.28 −3.55 −5.72

−4.71 −3.81 −3.31 −3.57 −5.79

112.70 −131.14 −198.14 −106.43 −142.64

11.78 −11.13 −13.32 −10.65 −12.32

69.02 61.91 88.88 56.48 75.83

−110.37 −129.48 −197.64 −105.91 −142.25

70.04 61.60 88.49 56.14 76.06

Note: The optimal lag used for conducting the Augmented Dickey-Fuller test statistic was selected based on an optimal criteria (Akaike’s Final Prediction Error), using a range of lags. The truncation lag parameter l used for the Phillips-Perron tests was selected using a window choice of w(s, l) = 1 − [s/(l + 1)] where the order is the highest significant lag from either the autocorrelation or partial autocorrelation function of the first differenced series. Relevant test equations and related technical descriptions for all unit root testing procedures are available upon request. Presented for levels tests only: ∗∗∗ , ∗∗ and ∗ indicate significance at the 1%, 5% and 10% levels respectively.